The policy gap

HOW IS POLICY IMPACTING RETAIL PROPERTIES AND WHY DOES IT NOT GO FAR ENOUGH?

CURRENT POLICY

As the negative effects of climate change are becoming more apparent, countries around the world are under increasing pressure to cut their carbon footprints. The UK was the first major economy that committed to a legally binding target of net zero emissions by 2050, but more progress needs to be made in issuing relevant policies to achieve this.

The UK government has developed plans to improve the energy efficiency of all retail buildings by mid-2035. However, there are significant gaps in the regulations, and policy has not provided the stability or long-term vision that will enable the industry to make a smooth transition to a low carbon economy. Rather than setting sustainability requirements, policy efforts that relate to commercial properties have been focussed on improving the standards of existing buildings.

While it’s critical to reduce the impact from buildings, there are still major barriers to retrofitting, identified by the UK Green Building Council, which apply across all sectors:

- High upfront costs, particularly for the newest technology

- A lack of finance mechanisms and a lack of a coherent offering for institutional investors

- No fiscal incentives

- Limited loan and grant schemes that have prioritised specific measures and prevented a whole building approach

- Insufficient capacity of materials, kit or personnel required to meet these targets.

Currently, most government funded initiatives are focussed on the residential sector. If it is not cost effective for the private sector to improve and upgrade existing stock, which a significant proportion of retail property is unlikely to be, are we at a stalemate, and how do we move forwards?

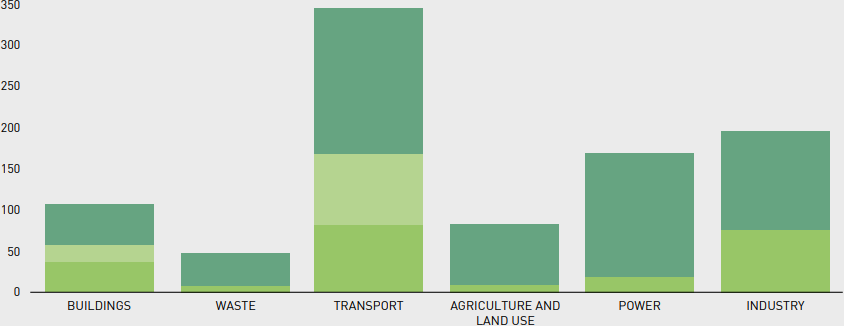

In its 2019 Progress Report to Parliament, the Climate Change Committee (CCC) stated that the building sector lagged behind other CO2 -intensive industries and recorded a mere 1% drop in carbon emissions between 2013 and 2018. Although the emissions subsequently plunged during the pandemic, the long-term outlook for the sector is uncertain. According to the net zero policy tracker published by Green Alliance in September 2021, current decarbonisation policies will only deliver a 36% cut in emissions needed to stay on track to net zero during the fifth carbon budget, which will run 2028-2032. Including effects of policies that are currently out for consultation would increase the reduction in emissions to just over 50%.

So, what are the key policies related to retail property and where are the gaps?

EPC, HEATING & MONITORING

The EPC policies setting the timeline for improving the efficiency of commercially let properties by 2030 will impact around 83% of retail property stock, but the details of the scheme still need to be refined. There are various issues with certification even before implementing improvement. For instance, the proposal is for commercially rented buildings to be EPC ‘B’ by 2030, assuming upgrades are ‘cost effective’. This appears to be a significant caveat, as financial viability is a major sticking point, and the cost of improved efficiencies will often not be paid back in fuel savings even over the long term.

Problems can arise where a landlord lets a unit in a stripped-out condition and the tenant’s fit-out decreases the final EPC rating below the level required by law. Given high demand for heating and cooling in retail, this could potentially be a common issue. The Department for BEIS1 will therefore need to define legal responsibilities of both tenants and landlords. Although the Government has announced its intention to support small and medium-sized businesses, few assisting measures have been taken. Meanwhile, fiscal incentives are missing, and available grants are tied to specific conditions and generally not fit for the purpose. There is currently no decarbonisation scheme for landlordoccupied non-domestic buildings even though they account for 60% of the nonresidential sector. Additionally, commercial buildings that are owned, not leased, are not covered by current EPC policy proposals, so who will be responsible to get these to grade if there isn’t any legislation to guide the process?

As the vast majority of buildings emissions result from heat, the Government has primarily focused on policies adopting low-carbon heating solutions. As part of its plan to only install clean systems in buildings from 2035 onwards, it has decided to start hydrogen trials from 2023, consult on the role of hydrogen-ready appliances and begin replacing fossil fuel boilers with electric heat pumps. In this respect, the Government has set an ambition to increase heat pump installations to 600,000 per year by 20282. However, the CCC warns this will not be sufficient to meet either the 2030 Nationally Determined Contributions (NDC) target or the Sixth Carbon Budget. The deployment rates in non-domestic sector remain low, running at less than 1,000 installations annually. It is currently unclear how the Government intends to motivate businesses to increase installations, given that the Renewable Heat Incentive for commercial pumps over 45 kW has been closed to new applications and partly replaced by the Boiler Upgrade Scheme (BUS) designated for domestic and small non-domestic buildings covering installations under 45kW3.

There are also clear problems with channelling policy on specific technologies at a time when significant innovation is underway and a more flexible approach is required. More attention needs to be given to the relationships between different initiatives: for example, the benefits from improved heating solutions are entirely negated if the buildings are not properly insulated.

Proper measurement of energy usage and efficiency is key to delivering on policy objectives. The Government has introduced a Performance-Based Policy Framework4 for large commercial buildings, requiring businesses over 1,000m2 to consistently report their energy performance. Data shows that there is almost no correlation between the actual performance of large buildings and their EPCs. This policy was therefore developed to establish a new way of assessing buildings’ energy consumption and close the ‘performance gap’. While the scheme will support building occupants to use their sites more effectively, and encourage investment into building fabric and systems, its scope is too narrow and improvement in performance is optional. It is also unclear when large retail players will be required to start reporting on their energy performance.

INSUFFICIENT MOMENTUM, SUPPORT AND INCENTIVE

The Government has made a significant step forward by publishing vital documents such as the Energy White Paper, Heat and Buildings Strategy, and the Treasury’s Net Zero Review. Yet the pace of the change is too slow and recent proposed policies do not match the size of the UKs climate change ambition. The Government has also recently published their Net-Zero Strategy - a key document that sets out the decarbonisation path for each sector. Although well-received and praised as “affordable and achievable”, longterm trajectories have been found to be vague. Subsector-specific plans and strategies, that would be particularly beneficial to retail, are also missing. Additionally, financial support in the form of loans and grants is insufficient, selectively applied and primarily focused on the residential sector.