Does residential work in town centres?

Development and sales activity would suggest that appetite for town centre living is stronger than ever.

An opportunity

The way we shop has impacted towns and cities up and down the country, some more so than others. Whether it’s Aberdeen or Chichester, they all have one thing in common, they are the heart and soul of our communities. These structural changes now give us the biggest opportunity to shape them into much better versions, fit for the 21st century. What happens next, matters. It’s arguably the biggest challenge facing the built environment sector.

As a member of Savills Residential Research team it probably won’t surprise you as to my diagnosis for what should happen next. Homes. Lots of them.

The good news? It’s already happening. Combining the retail boundaries of over 2,000 towns and cities across the UK, with data showing the delivery and planned delivery of housing, we can reveal how many homes are set to be delivered where the ‘retail core’ of towns and cities once stood.

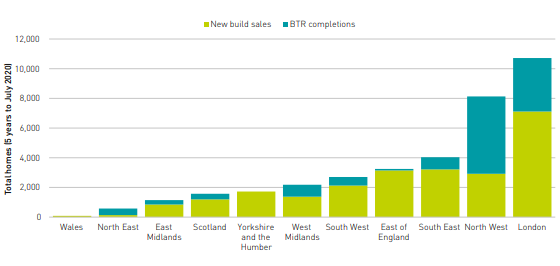

In the five years to June 2020, over 36,000 new homes were built in the very heart of our towns and cities. That is set to be eclipsed with a total of 68,000 new homes currently under construction and a further 173,000 with planning consent.

London unsurprisingly dominates recent delivery, particularly for private sales. The North West however isn’t far behind. Build to Rent has helped absorb a lot of stock, particularly in places like Manchester.

The time is now

Covid-19 has undoubtedly impacted the world around us, the built environment included. The truth is our towns and city centres were already changing. In 2020 these changes have accelerated. As the need for particular uses and businesses usually found in the heart of towns and cities reduces, opportunities arise to remodel and revitialise those places.

Whilst Covid-19 has given some the desire for countryside and green open spaces, for others it has meant convenience and being part of a community. The pandemic and its lockdowns have shown how human beings need to interact with other human beings. It is, after all, what makes us human. Our towns and city centres are the best places to make this happen.

A mix of uses

The American urban sociologist Ray Oldenburg once said “houses alone do not a community make”. This is of course true for many sprawling urban extension across the country. However, it should also ring true for how town centres should be looked at going forward. Just building homes isn’t the silver bullet to our town centres problems. Yes, they will help, but structural changes will mean the mix of uses in town centres will be very different.

The best way in which to make town centre uses more viable is to bring the people closer to them. In order to prosper, town centres need to provide a reason for people to visit, dwell and spend money in. Providing a mix of uses, much more than just traditional retail is needed going forward. That includes offices, schools, nurseries, doctors surgeries, as well a whole host of other uses on top of the usual coffee shops, barbers, bars and restaurants, alongside viable retail.

A mix of tenures

With small tight sites, conservation areas and listed buildings, on top of the general logistical requirements of building in a dense urban environment, developing in city centres has often proved tricky.

However, as larger sites come forward, such as shopping centres and car parks, the opportunities to deliver big wholesale changes, with a focus on housing has also increased. Investors with deep pockets who don’t wish for a quick return have pounced. Step forward, build to rent.

The sector is particularly suited to the centre of town. In fact 27% of all build to rent completions in the past 5 years have come from town and city centres. For new build sales, the equivalent figure is just 4%. Manchester is leading the way. Other emerging hotspots include Birmingham, Glasgow and Leeds.

Those investing in build to rent are investing for the long term. The mix of uses, the quality of the nearby environment and the community they create therefore really matter. After all, tenants are more likely to stay longer and pay a premium for the experience.

A mix of society

Analysis from Experian data of the largest towns and city centres, shows that in the retail core 35% of households are aged 35 and below. For the wider town centre this drops to 21%.

Whilst city centres of course attract a younger crowd for all that they offer, to be really successful vibrant places they’ll need to attract a breadth of society, both in terms of age, but also incomes and demographics.

That also includes retirement living. The recent refusal by Elmbride Council for a scheme in Walton-on-Thames for 222 new homes on the site of a derelict Homebase store was especially galling. The developer was Guild Living, a retirement living specialist backed by institutional capital from L&G. The council refused the scheme on the grounds that it would “undermine the vitality” of the town. This seems counter intuitive to the need to enhance town centre living across the demographic groups. We anticipate perceptions of the vitality of mixed generational living will become much clearer in time, with huge benefits.

Where next?

It is not just the big cities which will see new homes built in the centre. Yes it is most visible and prominent in places like Manchester and London, but as the data shows, smaller towns will also be delivering lots more housing in the very heart of their communities. Places just like Walton-on-Thames, but equally those with struggling town centres up and down the country.

Large developers have so far favoured large strategic sites in the major cities, but government funding initiatives are starting to increase the viability in smaller places and we are seeing an increase in appetite from niche developers seeking to tackle the challenges in smaller and regional locations.

Figure 7a: Town Centre Residential transactions

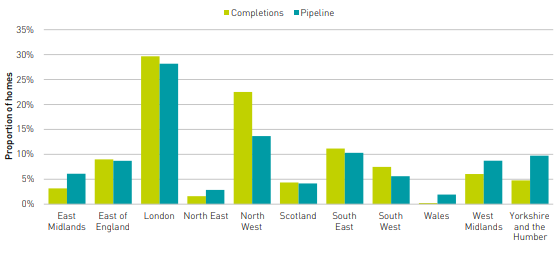

Figure 7b: Town Centre Residential Completions and Pipeline by Region

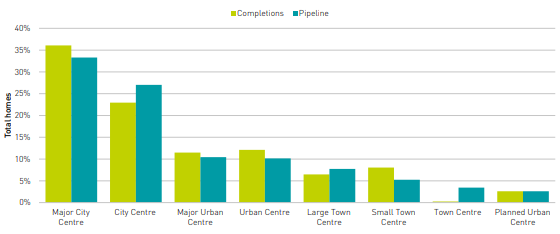

Figure 7c: Town Centre Residential Completions and Pipeline by Retail Place Type