But it can be complicated.

It doesn’t work everywhere. If the existing store is producing strong revenue, it is likely that continuity of sales and minimal disruption from construction will be important factors. Not all sites can allow for this.

A good example of a slow burner is the Sainsbury’s site in Ladbroke Grove, where Molior estimates capacity for c.600 new homes, yet there has been no activity to date. It is a sizeable part of an opportunity area, with canal frontage, and close to public transport. However it faces challenges around land ownership, and the developer needs to come to agreement with adjacent land owners in order to maximise the value effectively. It could be many years more before we see this site redeveloped.

There are other sites which initially look like they could be good opportunities, but yet have struggled to make any progress. One example is Sainsbury’s in Ilford, where planning has been obtained, but the land value doesn’t provide enough to deliver high rise residential on a podium, therefore this is likely to stay as a supermarket for now. This could change in the future when more people shop online and footfall decreases further.

The opportunity to reimagine retail isn’t limited to supermarkets. Other types of retail, such as retail parks and shopping centres, face the same pressure of reduced footfall from more online shopping and could make excellent mixed-use sites. Argent Related, British Land, Ballymore and Landsec are also all active in this space.

This is primarily an urban proposition and outside of London there has been an increase in this sort of development activity in recent years, but they are challenging. In the regions, the locations that have tended to favour supermarkets have rarely been those that favour high density residential. However, many supermarkets are now outdated stock, and a marriage with residential has the potential for them to update and improve the offer and cater for ecommerce, while residential footfall provides surety of trade and amenity for residents.

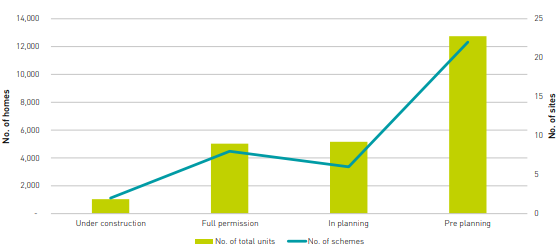

Figure 8: Existing supermarket sites, and planning status, where redevelopment into mixed use (including re-provision of a supermarket) is possible